This Week In Oil - April 26, 2020

I'm worried I'm being too negative...

Not much happened this week… I mean except WTI futures getting negative on the front month!

So what’s the story?

Just before the last trading day the WTI May’20 delivery contract traded negative for the first time in history. And not a little bit negative. On April 20 it traded all the way to -$40 per barrel.

Now let’s clarify. Two days before May’20 expires it is no longer the most traded contract. At that point in time most of the trading activity is taking place on the June’20 delivery. That means on April 20 the “real” price of oil was around $20 per barrel. Only a relatively small number of contracts traded at a negative value.

But why? The most likely explanation is that speculators who where long WTI on the May’20 delivery got squeezed by the hedgers with physical shorts ready to be delivered.

The thing is that you have two kinds of traders in the WTI futures market. The speculators who hold paper positions betting on price moves. And the hedgers or physical oil traders who are actually trading physical barrels of oil to be physically delivered somewhere.

In principle on the last couple of days before a contract expires the remaining market participants are all in the physical oil business. On Options Expiration day it is traditional to see most of the futures contracts being rolled to the new month with only the physical oil traders keeping sizeable positions.

But apparently this isn’t what happened this time.

Imagine you are not a careful trader. You are long the WTI May’20 contract and now comes the time to roll it. Your main issue is that WTI is in super contango. That means you have to pay a big premium - and lose money - to close your May’20 contract at a low price and buy a June’20 contract for +$5 per barrel higher.

So you might just think, oh I’ll wait as long as I can to roll, for sure the spread can only get smaller from there….

No. After the May’20 Option Expiration day which was on April 16 if you are not out then your paper long positions are facing physical oil short positions. And given how expensive storage is these days nobody short physical oil is going to take those barrels of your hands. They don’t need your oil, they already want to get rid of theirs.

So what happens for those few traders that are left holding long paper positions just before the last trading day? They get squeezed by the physical traders. And this is how you get prices dropping all the way to -$40 per barrel.

This was basically a technical squeeze that only affected a very limited number of contracts that were not on the active month. And the underlying theme is the scarcity of storage capacity in the US since demand evaporated.

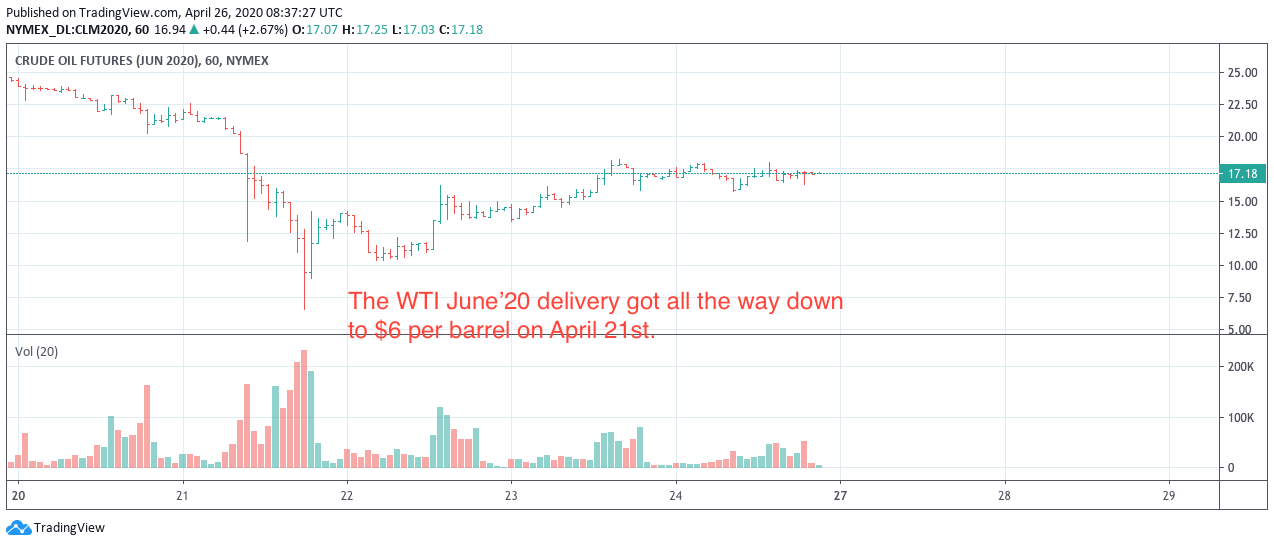

But more interesting is was happening on the active contract on April 21.

The June’20 contract held pretty well around $20 during the whole negative prices episode on the May’20 delivery. But the next day it went all the way down to $6 per barrel on big volumes.

That was real. That wasn’t a technical squeeze. And apparently this crash was triggered by the USO fund.

Recently a lot of people got the bright idea to just buy shares of the USO ETF. Their bet is that for sure this oil price can only be temporary. So buy USO now while the oil price is negative and profit later.

Except this is not so bright when the market is in super contango as the cost of rolling positions almost guarantees you are not going to make big money on that.

USO decided they don’t want to be caught in the same technical squeeze that gave us negative oil prices this month. And to prevent that they have aggressively sold their long positions on the WTI June’20 delivery to buy months further down the curve such as July and August. This put a lot of pressure on the June’20 prices and got use down to $6 for a brief period of time.

At the end of the week we were back at $17 per barrel.

Anyway I’m going through all that to show that people are spooked. No one can escape the reality that storage capacity is now a real issue.

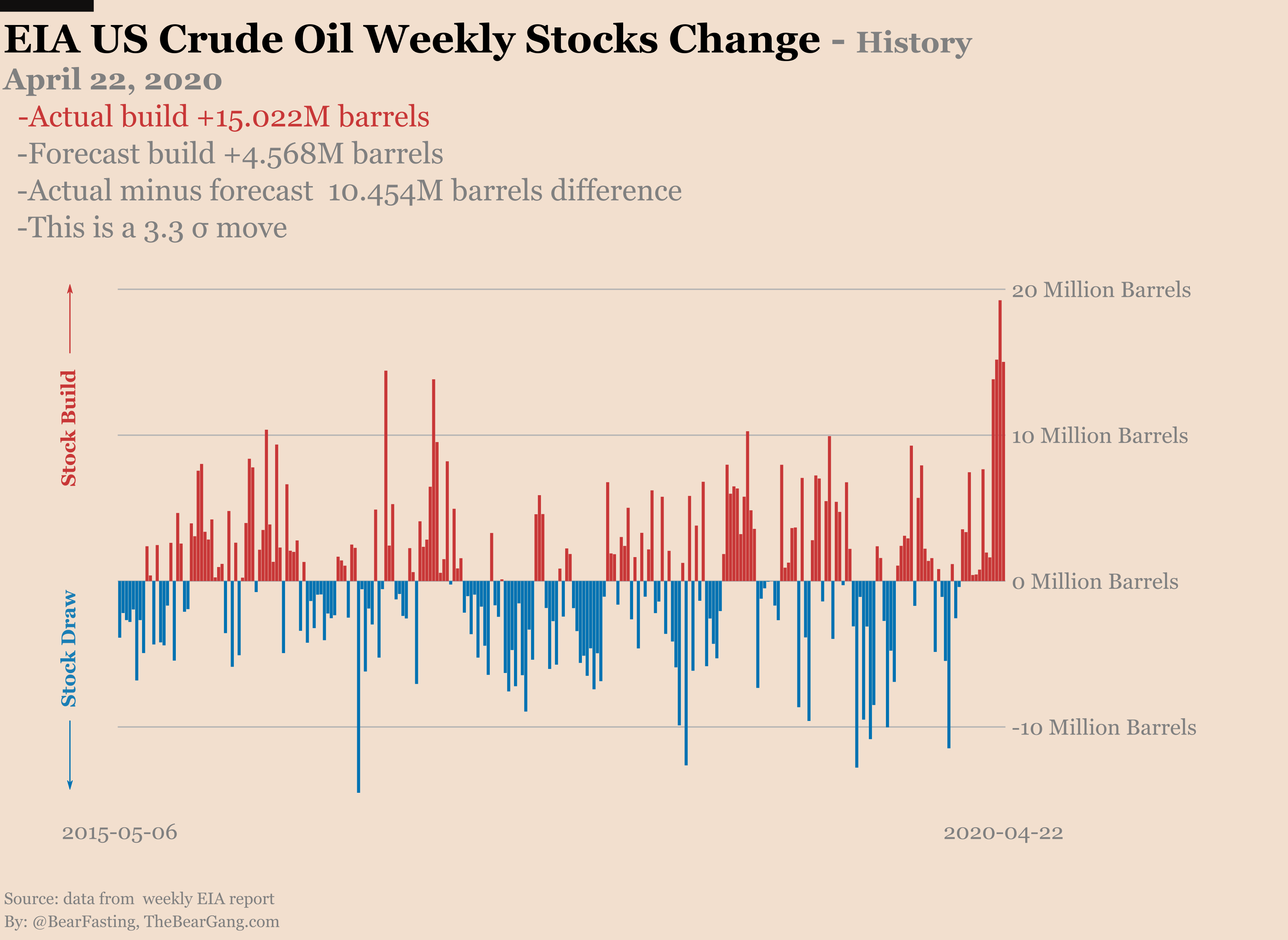

And the data we had this week shows this isn’t getting better.

The EIA reported a build of +15 million barrels. Once more staying close to record high numbers.

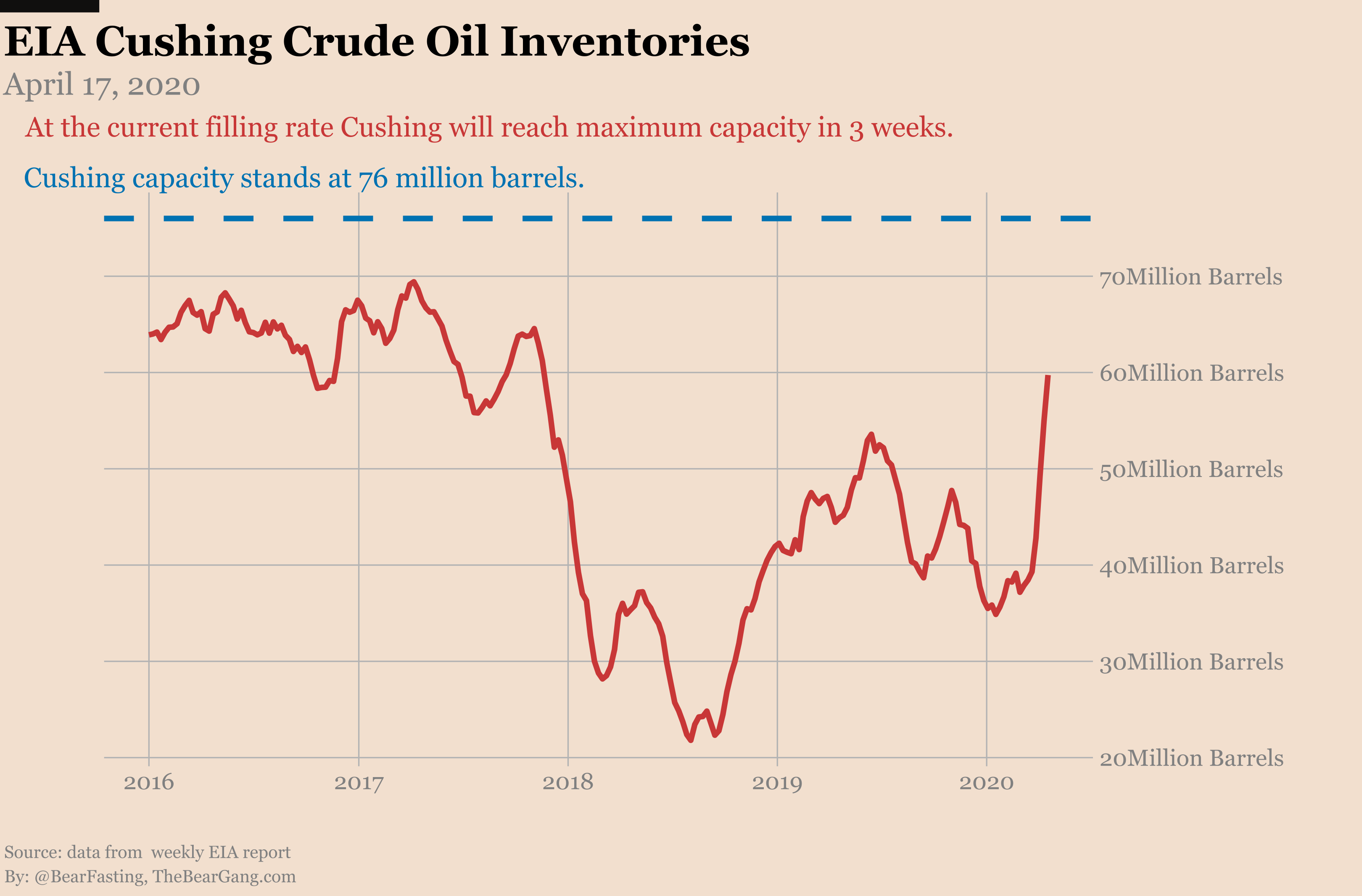

The problem is especially bad at the Cushing delivery hub with another +5 million barrels build.

There are now 60 million barrels of oil stored in Cushing. At the current filling rate it will be completely full in 3 weeks.

The real question is how long are we going to be in trouble. I mean surely the US won’t be in lockdown forever. Demand is going to come back. And naturally production is going to decline which means supply and demand will get more balanced… right?

Well the real answer is that nobody knows. The global supply chain is badly damaged. Unemployment in the US has skyrocketed. A lot of companies are going bankrupt. And there is always the risk that the world will get a second wave of the coronavirus.

We could be seeing low oil prices for a while.

At least this is what suggests the WTI term structure. The curve is still in super contango and it is getting steeper. We now have spreads of more than $0.50 between consecutive months up to January’21.

That is as far as the market is pricing disruption at the moment…

We might not get another technical squeeze that will bring WTI in the negatives but keep an eye for prices moving below $15 consistently.