This Week In Oil - June 14, 2020

I have bad news...

Well that wasn’t such a good week for oil after all. After seeing a very impressive rally fuelled mostly by high hopes and wishful thinking it looks like oil is coming down to earth. I guess it is true that you can’t ignore the fundamentals forever.

So there it is, after a month of gains we have our first weekly loss in a while on WTI.

You are forgiven if you thought that after the OPEC decision on extending its production cuts WTI was going to push over $40. That’s an honest mistake.

Instead things went the other way and we end up $4 lower around $36 at the close on Friday.

What are those bad news that I’m talking about? Let’s see:

Higher inventories

Production levels in the US that are likely to have bottomed

Demand remains weak

Bad outlook for the US economy and the global economy

Resurgence of COVID19 cases

Yea, that’s pretty much everything that has been making me doubtful about this rally for a while now. But let’s go through these one more time.

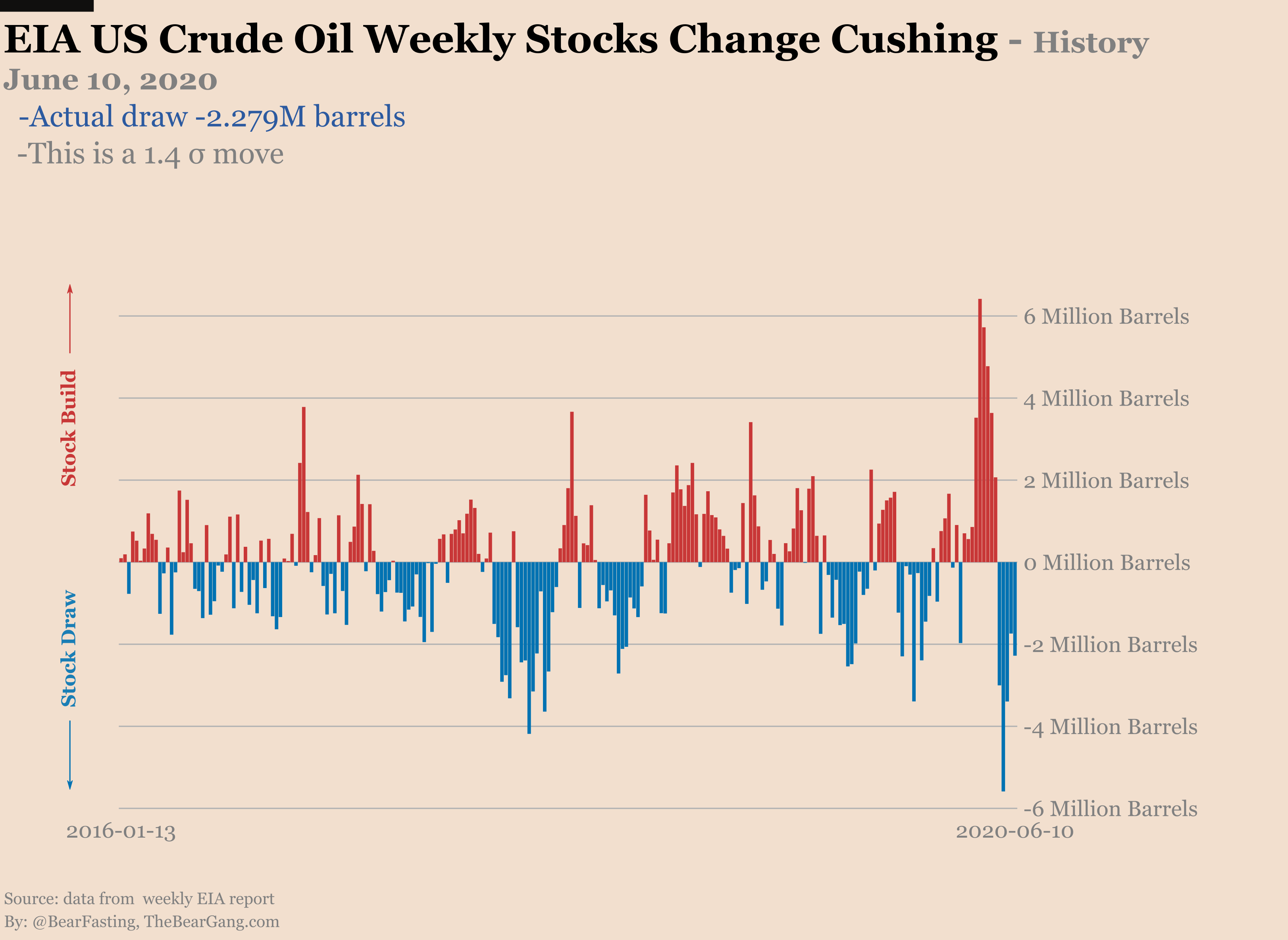

This week the EIA report is showing builds:

Total US Crude +5.720 M this is a 1.2 σ move

Cushing -2.279M this is a 1.4 σ move

Gasoline 0.866M

Distillates 1.568M

Thanks to all the oil floating around the world inventories are not getting lower. It will be a while before we work through all that extra capacity. Sure right now there is no storage crisis. But that doesn’t mean inventories are low either!

The rate of the production cuts is getting slower. The US production is just over 11M barrels per day. When everything is settled and we have more accurate data I’d guess the bottom will be in the range of 10M to 11M barrels per day. The EIA forecasts this bottom to be around 10.6M barrels per day with the production for the year averaging 11.5M barrels.

That will of course depend on the price action. As long as WTI stays above $35 we will see production start climbing up again.

For the demand side you just have to glance at the economic outlook from the Fed to see that there is no V-shape recovery in sight. Let me summarize that with one number: 9.3%…

This 9.3% is the forecast for the unemployment rate in the US at the end of 2020. That’s about the same as the unemployment rate at its maximum after the 2008 crisis!

Is that supposed to be a V-shaped recovery?

With so much damage in the real economy it makes no sense to assume that there won’t be long term consequences on the oil demand.

And that’s without taking into account a second wave of COVID19. For now Texas, Florida, Arizona and California are reporting what could be the start of a second wave of the coronavirus pandemic. How long until that leads to a second wave of lockdown? How many businesses can survive that?

And by the way this isn’t only about the US. Beijing also recently reintroduced partial lockdown measures after a new spike in cases.

Most people are acting like this pandemic is over, but the number of daily new cases worldwide is still increasing!

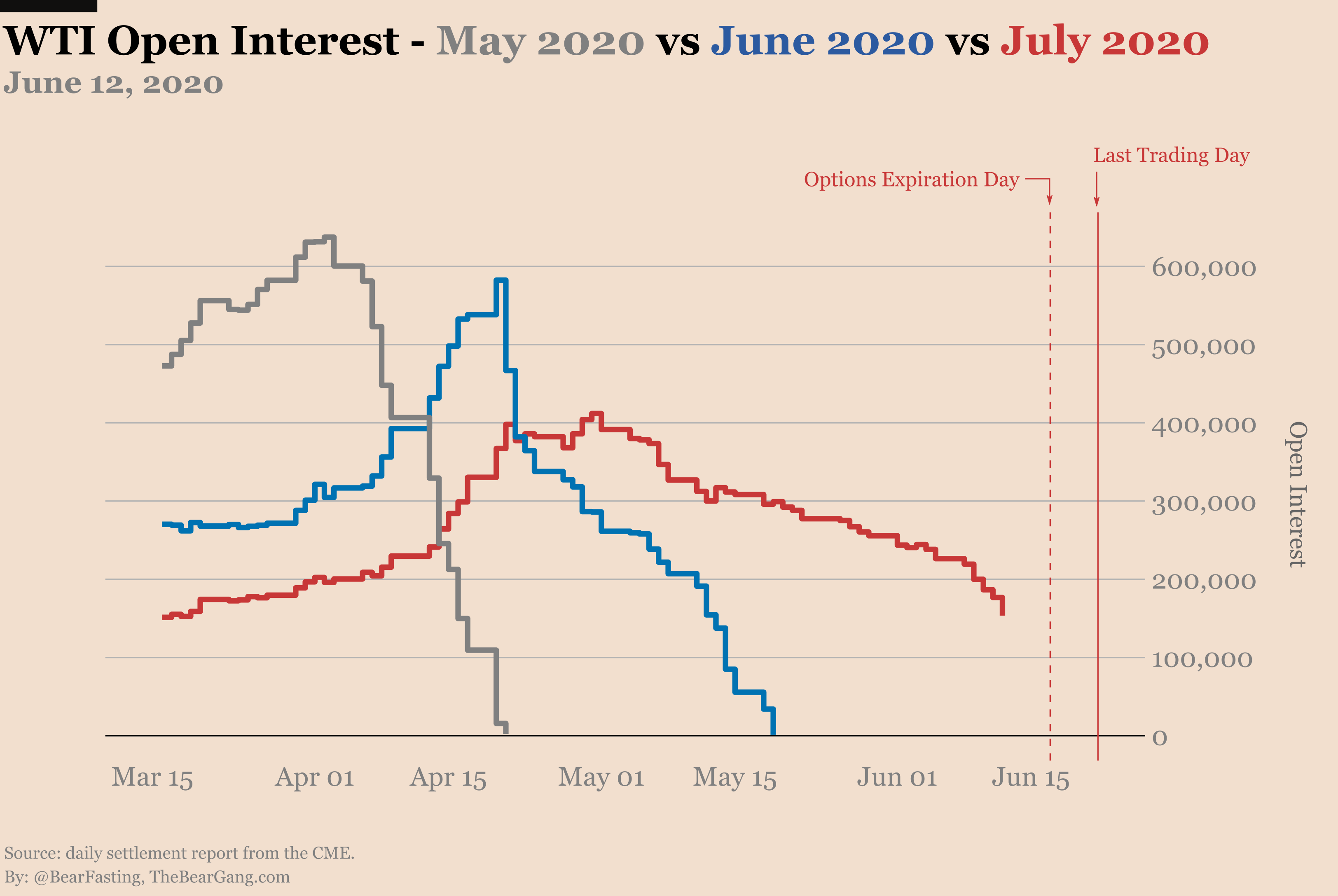

June 17 is options expiration day and June 22 is the last trading day for the WTI July delivery. We’ll have to see how that plays out but there is no indication that we are heading for a technical squeeze such as the one that led to negative oil prices in May.

Best to keep an eye on it though.

In the meantime let’s keep our eyes open for a change in narrative about oil. Bad economic outlook, resurgence of COVID19, the more those topics take centre stage in the news the closer we get to a strong correction in oil prices.

If you liked this article please subscribe and share!