This week in Oil - June 22, 2020

It's all a misunderstanding...

Maybe I’m getting it wrong. I don’t know. But the way most traders are looking at the big picture doesn’t make much sense to me. I say most traders because if that wasn’t the case this WTI rally would have tanked this week.

Instead we are sticking around $40 per barrel.

Reminder that the last trading day for the July delivery is today (June 22). Judging by what happened since OpEx last week there is no reason for any fireworks this month.

So let’s take a step back and think more long term. Let me list a bunch of facts that we learned last week:

Fact 1: the US production is down.

Fact 2: total US inventories are up.

Fact 3: the second wave of COVID19 is a real thing.

Fact 4: even according to the EIA the demand recovery is going to be very slow.

Apparently when the oil market sees that the narrative is production is down so much that we when the recovery happens we’ll be short of oil…

How about a different interpretation? Let me give it a try.

The US production has been in a correction phase to adapt to the crash in demand. Despite production being down the total US inventories still manage to climb up! That means there is still too much oil in the system given that the recovery of demand will be slow. Moreover the risk of a second wave of coronavirus causing further damage to the US economy is high.

What do you think about that? Certainly this is not bullish for WTI.

Sure the US production is down to 10.5M barrels per day. But prices around $40 are good enough to restart production for many operators. I still think that, bar a second wave of lockdown, we have found a bottom. There is definitely capacity in the system to move us back above 11M barrels per day relatively quickly.

So in the short term I don’t see how those production figures mean we’ll run out of oil. If market forces have pushed production down during the storage crisis then they can correct the other way when production starts generating profits again.

And talking about storage crisis there is something I can’t really wrap my head around. Check out the time spreads. The market is getting really tight.

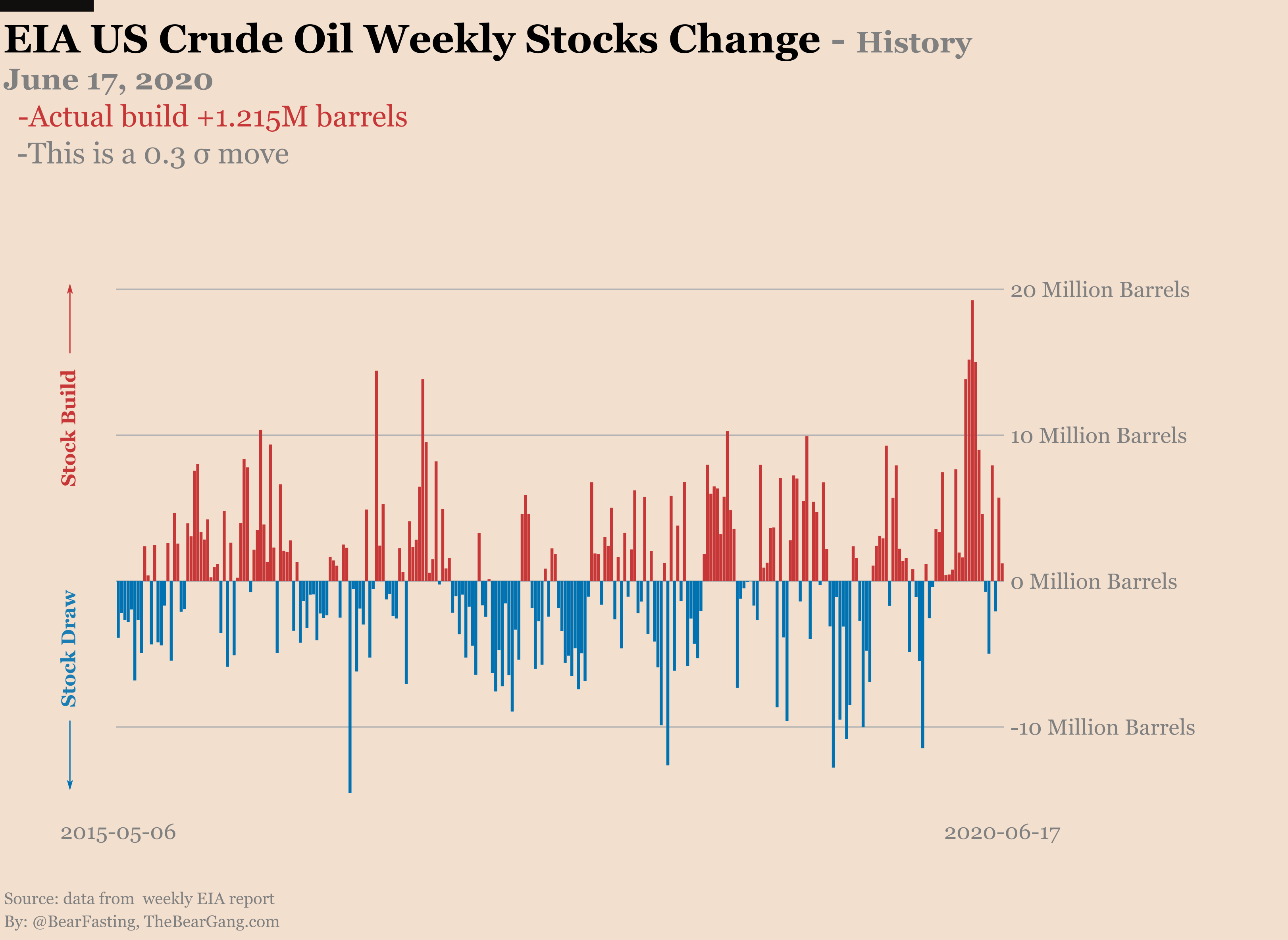

But at the same time the EIA stocks report for the week gives:

Total US Crude Oil +1.215M barrels, this is a 0.3 σ move

Cushing Crude Oil -2.608M barrels, this is a 1.6 σ move

At the same time:

Gasoline -1.667M

Distillates -1.358M

Ok, sure, Cushing is continuing to draw. But most of it is likely to be going to the US Strategic Petroleum Reserve. Remember that now the SPR is leasing some of its capacity to commercial oil.

The thing is most stakeholders have very little appetite for a second round of negative WTI prices. The safe play for them is to have Cushing inventories move the SPR. This way they make sure there is always space left in Cushing to avoid another crisis.

While Cushing is drawing you can see that the total US inventories including SPR continue to rise. As a matter of fact, except for a short blip down a few weeks ago the trajectory is still firmly on the upside.

There is so much oil in the system that I honestly don’t see how we could get rid of it so fast. I mean it is not like the real economy is doing great… hence the mystery of the time spreads…

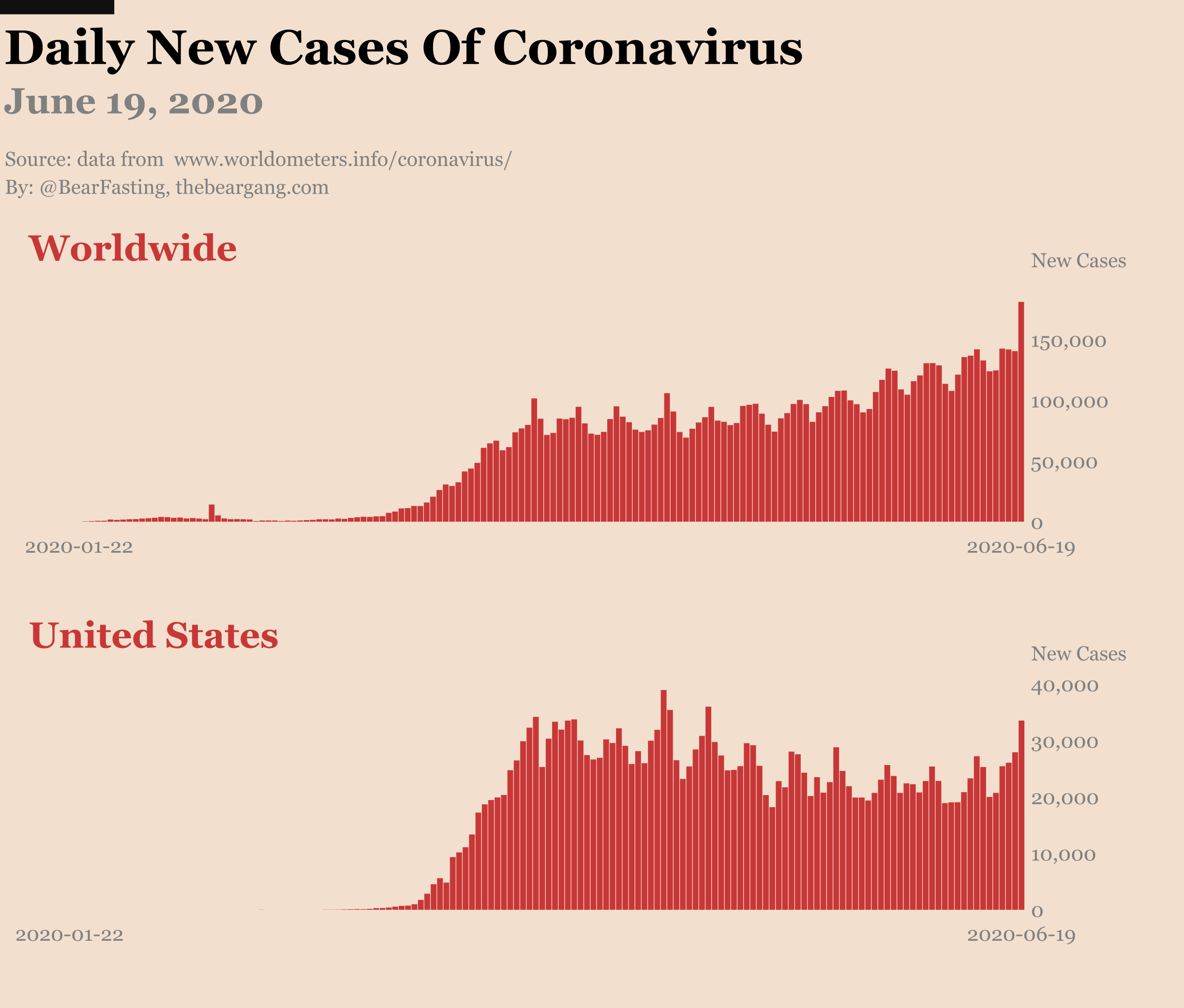

Finally there is this coronavirus story. It seems that for some time people forgot about it. If you look at the number of daily new cases though it is looking worst over time.

Worldwide the trajectory of the curve is upward. At no point in time did it move down. Different parts of the world are affected at different times sure. But overall this is not under control.

For the US it looked like things were getting better with a slow downward slope. But no. Now it looks like we have a second wave on our hands.

Remember what happened for the first wave in the US. It all started with denial. Nohting to see here. Then all of a sudden it became a problem, the economy tanked and the country got put on lockdown.

I wouldn’t discount this happening a second time. Better be prepared…

If you liked this article please subscribe and share!