This week in Oil - June 28, 2020

Catching up with the fundamentals…

Sometimes I feel like I repeat myself a lot. But really it’s not my fault if the oil market is taking forever to catch up with fundamentals.

The bulls have tried to push WTI much above $40 but that didn’t last very long. At the end of the week we are back down to $38.

The reason? A slow change of narrative. We are moving away from fantasies of V-shape recoveries and over optimistic projections for oil demand.

And it isn’t like the reality of the situation was particularly hard to see.

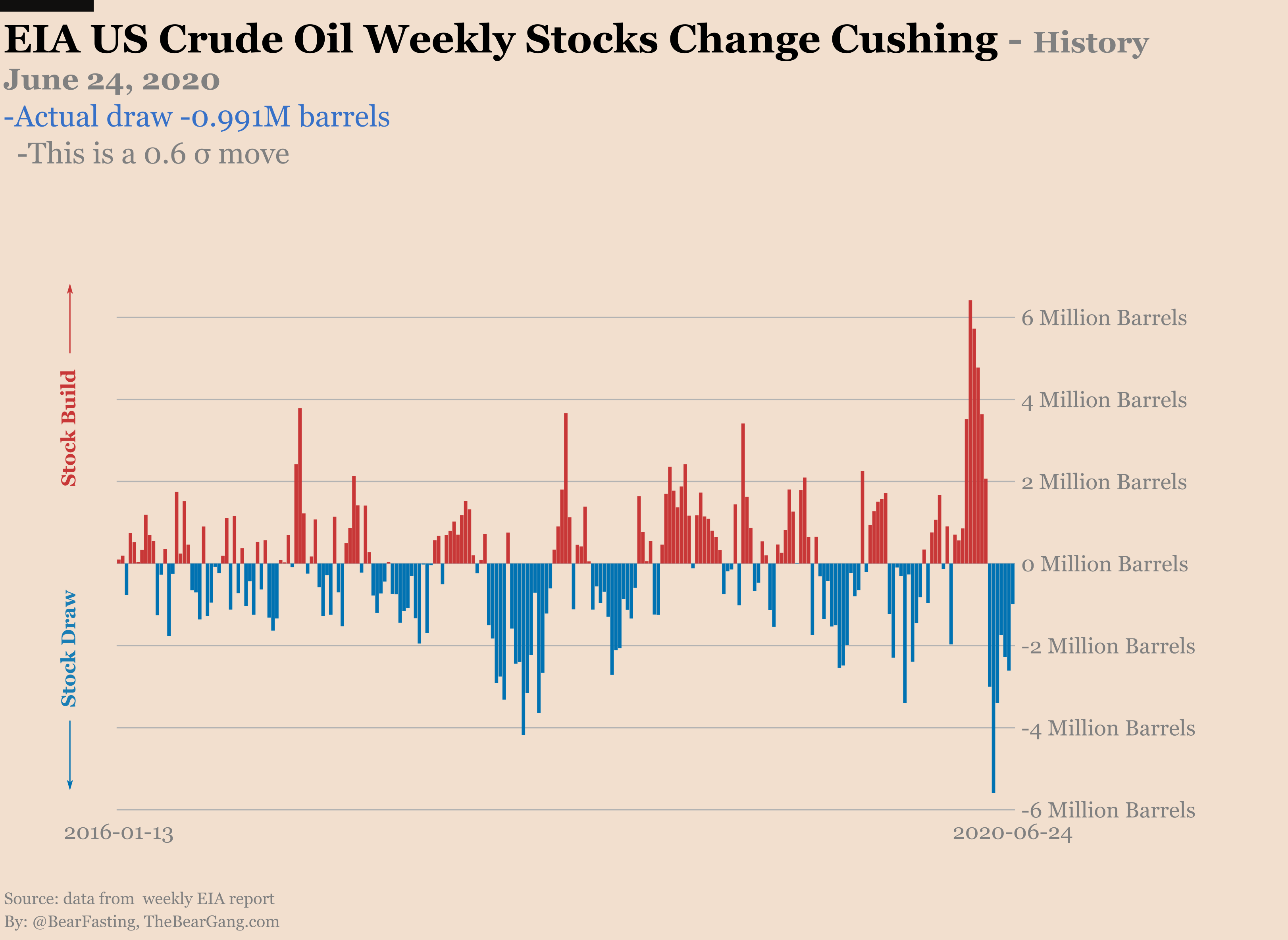

We all remember the storage crisis. It was so acute that it created a paper long WTI squeeze which resulted in oil futures going negative. If you look at the time spreads today you’d think this is completely gone. Check out that market. Pretty tight right? You could bounce a quarter out of that spread.

But when you peek at the actual storage data things aren’t looking so good. Cushing is still drawing almost 1M barrels this week. Ok. Honestly that’s not a very big draw. Most of it is probably going to the commercial storage leased at the US Strategic Petroleum Reserves anyway.

Meanwhile the total US crude oil stocks continues to build. +1.4M barrels this week according to the EIA. Since the beginning of the crisis there were only three weeks of draw at the national level. This is starting to pile up pretty high.

Now why are the time spreads so tight given that in terms of storage we haven’t really made much progress? I’m not completely sure. What that’s supposed to tell us is that there isn’t any physical storage play to arbitrage. That’s probably a result of the SPR leasing capacity for commercial use. This extra capacity is used to make space in Cushing which keeps the storage issues out of the spotlight.

But still, inventories are building.

So even if there is no acute storage crisis there is still plenty of oil in the system. And up to now the demand recovery which followed a reopening of the economy is at a plateau still well below full recovery.

How are we going to get rid of this glut then… yea, I don’t know either!

The fact that the US production has bottomed at 10.5M barrels per day is not going to help.

I’ve already talked about that before. WTI moving back above $35 is good enough to push production to restart. That means more oil in the system and starts a new cycle oil producers game theory.

Rest assured that OPEC+ don’t want to give up on market share in favour of US producers. So who knows how long those OPEC production cuts will really last.

Finally demand path to recovery is more fragile than the mainstream narrative would have you think. For now demand has plateaued. But what about the thing that started all that?

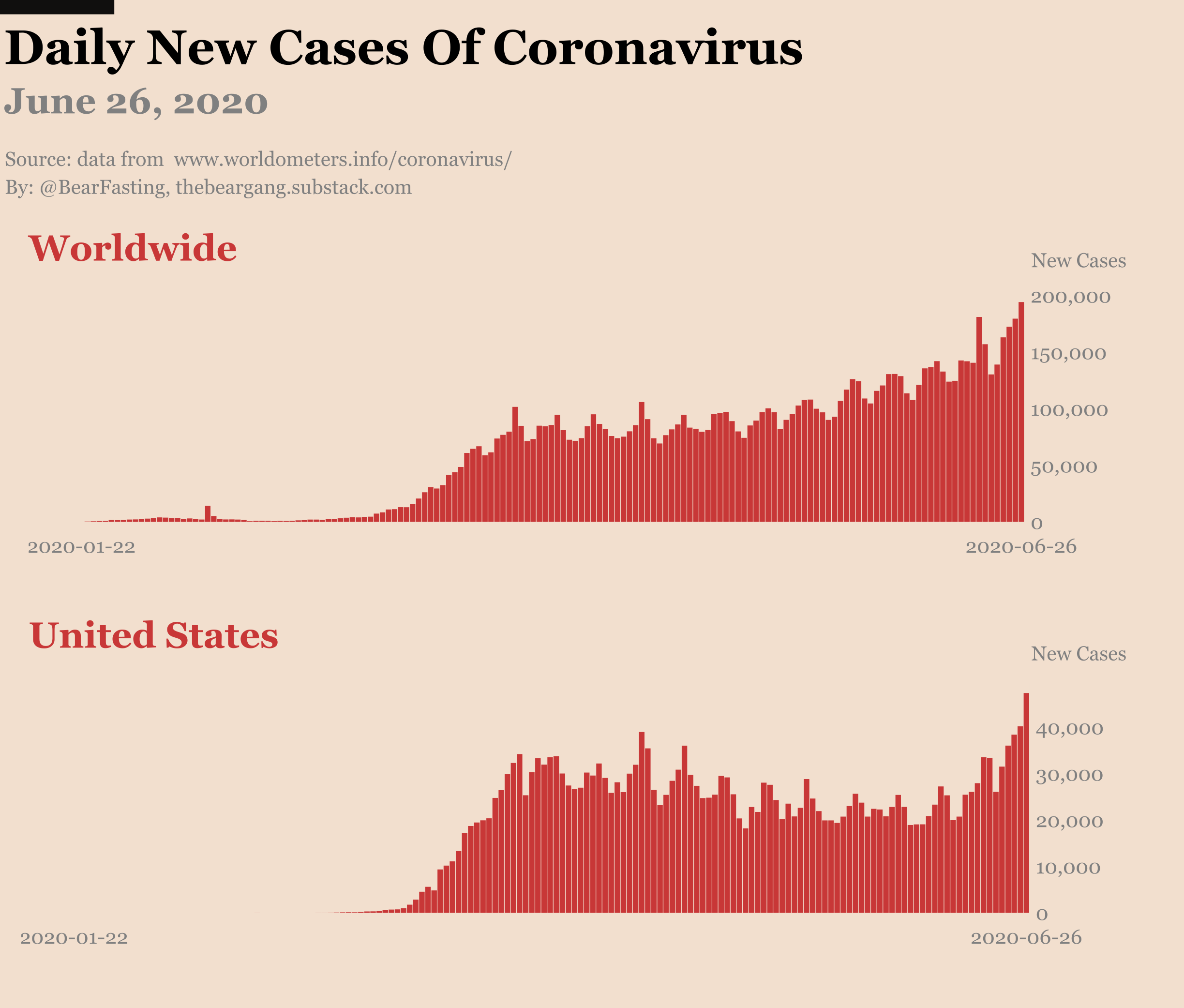

Yes the thing. You know. The thing that the markets have decided to ignore over the past few weeks. Yea that one. The coronavirus pandemic…

If you look at the oil market or the US stock market you’d think this is all done. But ffs, just look at the curve of daily new cases. That thing ain’t over.

Worldwide we never saw a downtrend in the number of daily new cases.

In the US it looked like things were slowly going away until BAM!?! the second wave is upon us.

Right now we are breaking new record high number of daily new cases in the US and worldwide. Some states reopening too fast combined with the protests across the country are certainly fuelling all that.

But the result is the same. Texas, California and others might be back on full lockdown pretty soon. So basically we are back to square one when it comes to demand destruction…

So yes, the WTI rally has stalled. But when you consider that:

Storage continues to get more full every week…

Production is at least already past its bottom…

Demand is weak and about to get weaker with a resurgence of COVID19…

only one thing comes to mind…

If you liked this article please subscribe and share!