This Week In Oil - May 10, 2020

Waiting for OpEx...

I feel like to understand a market you need to look at three aspects:

The fundamentals.

The technicals.

The narrative.

The fundamentals are in control over the long run. In the end they always bring the market back to reality. But in the meantime we can’t ignore crude oil technical setup and the narrative driving the traders’ sentiments.

Fundamentals

Well in terms of the fundamentals we continue to have an oversupplied market, a sluggish demand and a storage crisis. It has been like that for a while now. No big surprise coming along this week.

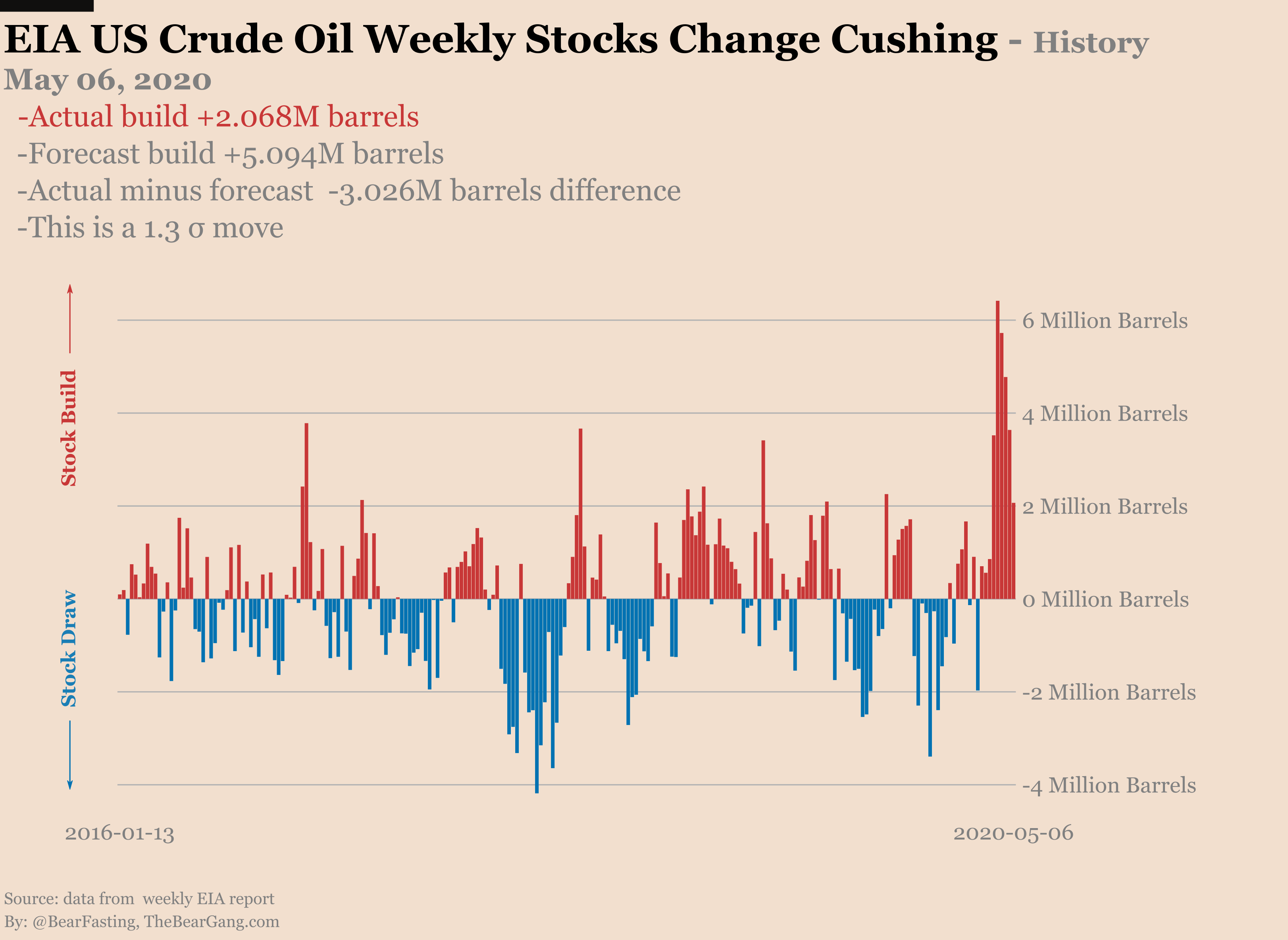

The EIA reported yet another build. Smaller than the previous ones but we expected that.

Let’s focus on Cushing:

Actual build +2.1M barrels

Forecast build +5.1M barrels

This is a 1.3 σ move

Taken alone a 2M barrels build would be considered large for Cushing. But when compared to previous weeks it looks small. We have already talked last week how this is the wrong way to look at things so I won’t come back to that.

That build is putting Cushing inventories at about 86% of their capacity. In practice taking into account logistical issues we’ll never reach 100% full capacity. At best we’ll get to 90-92% and call it a day. We are getting close to that.

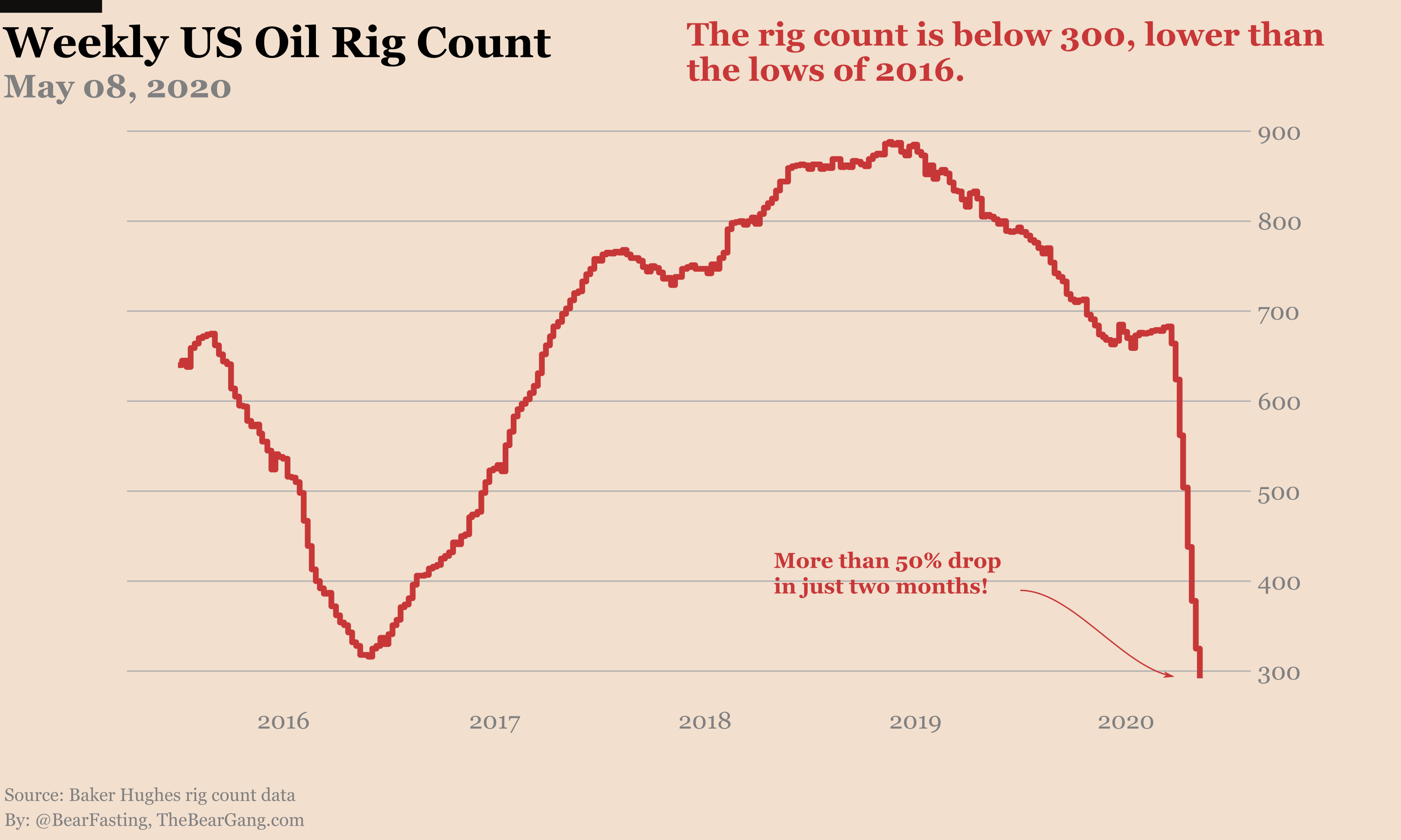

To be fair the low physical oil prices and the logistics of storage have forced the production to come down. We are seeing record fast drop in rig count week over week. And the overall US production is trending down. It went from 13M barrels per day a month ago to less than 12M barrels per day now. That’s a rate of about 200,000 barrels per day less every week.

Who knows where is the balance between supply and demand though?

Sure economies are starting to reopen but a lot of damage is already done. A V-shaped recovery feels like fantasy. That means production will probably continue to adjust downward in the next few months.

And that’s without counting the time it will take to draw from the storage that are virtually full both inland and floating.

At the current rate it would take a couple of months to reach 10M barrels per day. Certainly a strong psychological level.

Technicals

Remember what happened last month. The fundamentals pushed WTI down to the teens. But the negative price was a technical issue.

When options expiration day happened last month we were left with an imbalance between the paper long traders and the physical oil short positions. Just before the last trading day paper longs had to be liquidated and they got squeezed by the physical shorts.

Is it going to happen this month? You’d think that this is less likely to happen. The memory of the previous month debacle is fresh in everyone’s memory. Most likely people won’t get fooled twice…

Maybe maybe not.

Compared to last month the spread is much smaller. This Friday we are sitting at $1.6 on the front month compared to $7 after options expiration (OpEx) day last month for the May delivery. Although much more expensive than in normal situations that kind of spread is reasonable enough to not hesitate rolling your long positions early.

So there are less reasons to find anyone with no business still being in the market after OpEx on the June delivery.

But there is something new this month. Many investors, mostly retail, have seen the headline of negative oil price. And they have made the calculation that for sure oil can only go up from there. Their move to capitalize from that? Buy an ETF such as USO and wait for oil prices to go back up.

Sadly they missed the fact that those funds are long oil with WTI futures. And in a super contango situation the spread will suck away all your profits…

Regardless that means there was a big influx of money into those funds. Which in turn translates into more long paper oil futures positions.

Now USO is not run by idiots and they know that this big influx of money is going to be a problem for them if they keep all their contracts at the front of the curve. So after the scare of negative oil prices on the May delivery we can see that a lot of positions have moved further along the curve.

At 4 days of the OpEx for the June delivery we are left with about 200,000 open contracts. I’d expect that when OpEx hits this month we’ll end up with less open positions than last month. If that’s the case then it should not be as bad as last month. Still I would not be surprised to see low teens prices for June.

But if for some reason we don’t see a sharp reduction in open interest then another squeeze is possible.

The narrative

What is the current dominant narrative? The ingredients are the following:

Production is in free fall and storage is not a problem anymore.

Economies are reopening so demand is going to increase.

We are past the peak of the COVID19 pandemic crisis.

The bottom is in.

This is what’s driving the rally from $10 to $25.

Is this rally overdone? I think so.

The main issue remains that oil inventories are getting closer and closer to full capacity. Production is slowing down but nowhere fast enough to compensate for the lack of demand. And while we are going to get some sort of demand recovery when the economy reopens it will be far from where we stopped. A V-shaped recovery is not in the cards. The future remains uncertain.

This week we need to watch out for options expiration day on May 14. How many positions remain open after that and at what spread with the July contracts will tell us if traders have learned their lessons.

Let’s see how that plays out!

In the meantime if you liked this article please subscribe and share!