This Week In Oil - May 17, 2020

Rebalancing the market...

So what’s the story?

In the past few weeks the market for oil looked really bad.

Storage capacity became very rare and pricey. The coronavirus pandemic put the world’s economy on lockdown. Demand for oil evaporated overnight. The price of WTI fell down to the teens. This culminated with negative oil prices in a long paper oil squeeze on the WTI May delivery.

And what happened next? Let’s look at the data.

First of all the super contango is gone. In three weeks time we went from a $2.5 spread on the front month back to a normal range. Check out the sequence.

That means the WTI futures are not pricing any issue with storage in the next six months. We went from spreads indicating that storage capacity is virtually full for the next few months back to normal. Just like that.

That was quick!

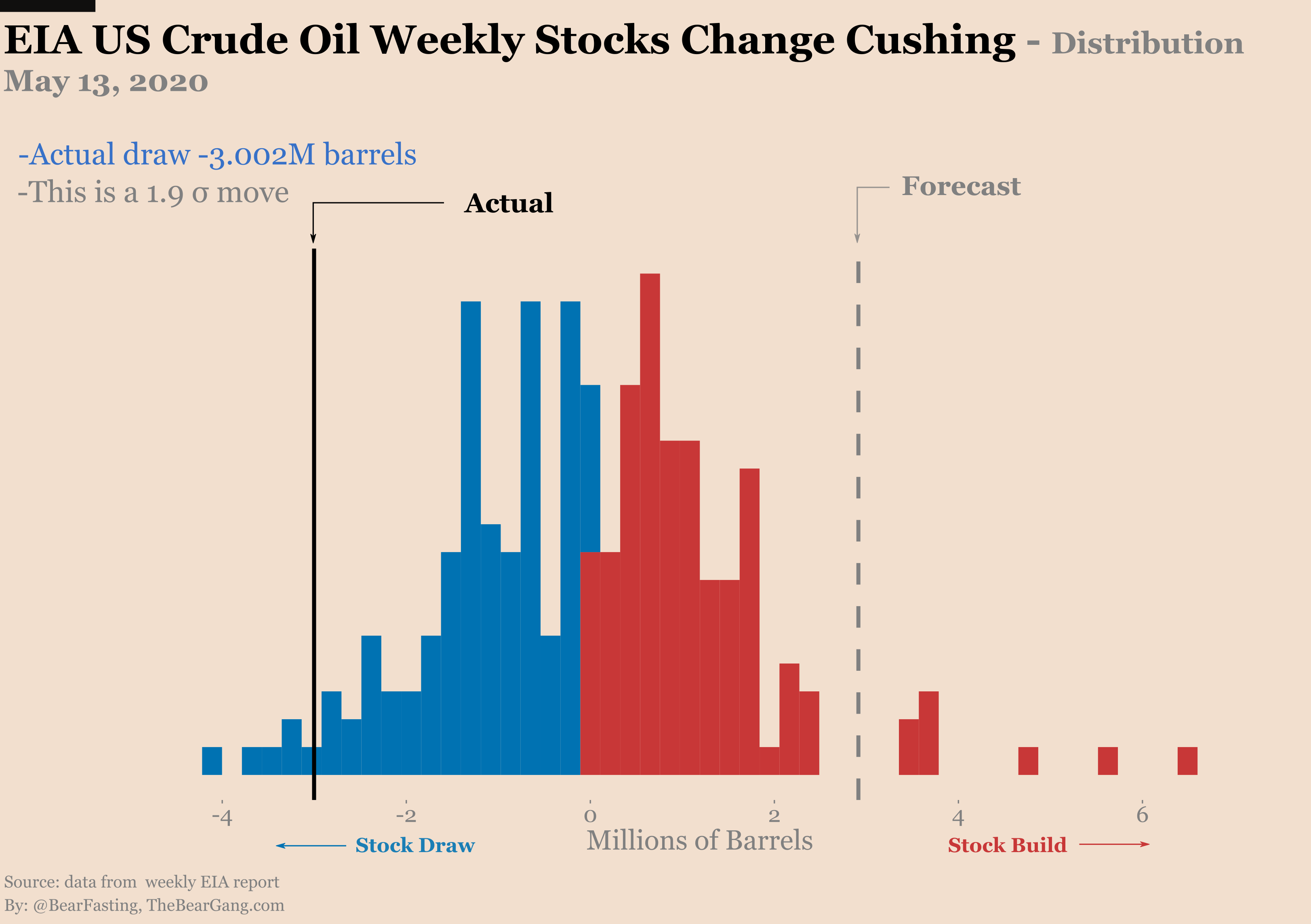

That trend already started in the previous two weeks but it got reinforced after the EIA US oil stock changes report. For the first time in a while Cushing started to draw. And historically speaking that’s a big draw:

Actual draw -3M barrels.

This is a 1.9 σ move.

To some extent some of it must be purely technical. With tanks almost full there wasn’t much space to add more so you’d expect inventories to come down at some point. It went down more than I expected but the important thing is the trend, is it going to draw more from there or was it a one off technical thing?

We shall see.

Note that even after a -3M barrels draw inventories level at Cushing remains high.

For the US as a whole we’ve seen only a small draw of -745k barrels.

But really this one data point from the EIA report does not make for a convincing story regarding storage capacity coming back to normal. There must be more to it right?

We are standing on three pillars:

Storage.

Production.

Demand.

The storage story is kinda weak. Especially when you take into account the amount of floating oil in tankers all over the seas right now. Let’s turn to production then.

The rig count continues to fall. Down 60% since the start of the coronavirus pandemic crisis. In other words shale oil is being decimated! Sure that’s a lot of production coming offline but we should not underestimate the capacity of shale oil to spin production back up really fast if they sniff demand coming back.

But overall the US oil production is taking a big hit. If we continue that trend we might be at or below 11M barrels per day within a month.

That checks out as something that would move prices higher. So here is a six points narrative for you:

Production has been severely impacted by the low prices and high cost of storage.

Together with OPEC+ cuts the rebalancing of supply already happened.

Now that the worst of the coronavirus pandemic is over in the short term demand will start drawing the storage glut.

So the time spreads should get tighter.

And in the long term when demand fully recovers there won’t be enough production.

So prices should go back up.

Does that sounds familiar to you? This seems to be the dominant sentiment in the market and you see that reflected in prices. And this is actually quite a plausible scenario painted here.

There is one problem though. A bunch of assumptions are baked in to make this work.

First we are all acting like the coronavirus pandemic is behind us. Sure many countries are past the peak of infections. But it will probably take months to get back to levels of daily new infections that are so low that all restrictions can be lifted.

Now what about the chance of a second wave? If that happened we’ll be up for a second round of lockdown. More demand destruction. And also an increasing likelihood that we could see travel behaviours changes as well as changes in the logistics of the global supply chain.

The first order effect of the coronavirus pandemic is the lockdown. This is direct and forced demand destruction. But the second order effects will have more lasting effects. How many businesses are failing? How many people are going to be durably unemployed? Are we heading for another depression?

It is now too early to know how big those effects are going to be but we can’t pretend with a straight face that we’ll have a V-shaped recovery.

Which brings us to the issue of production. With demand in the dumpster and prices historically low the market is being forced to cut production. This is true in the US and it is also true for OPEC+. But as demand is slowly starting to come back you can’t trust that to continue. Will shale oil restart with a bang? Which member of the OPEC is going to start cheating on production quotas?

My point is that this six steps narrative for why oil prices are going to skyrocket might also be a setup for failure with so many uncertainties for the rest of the year.

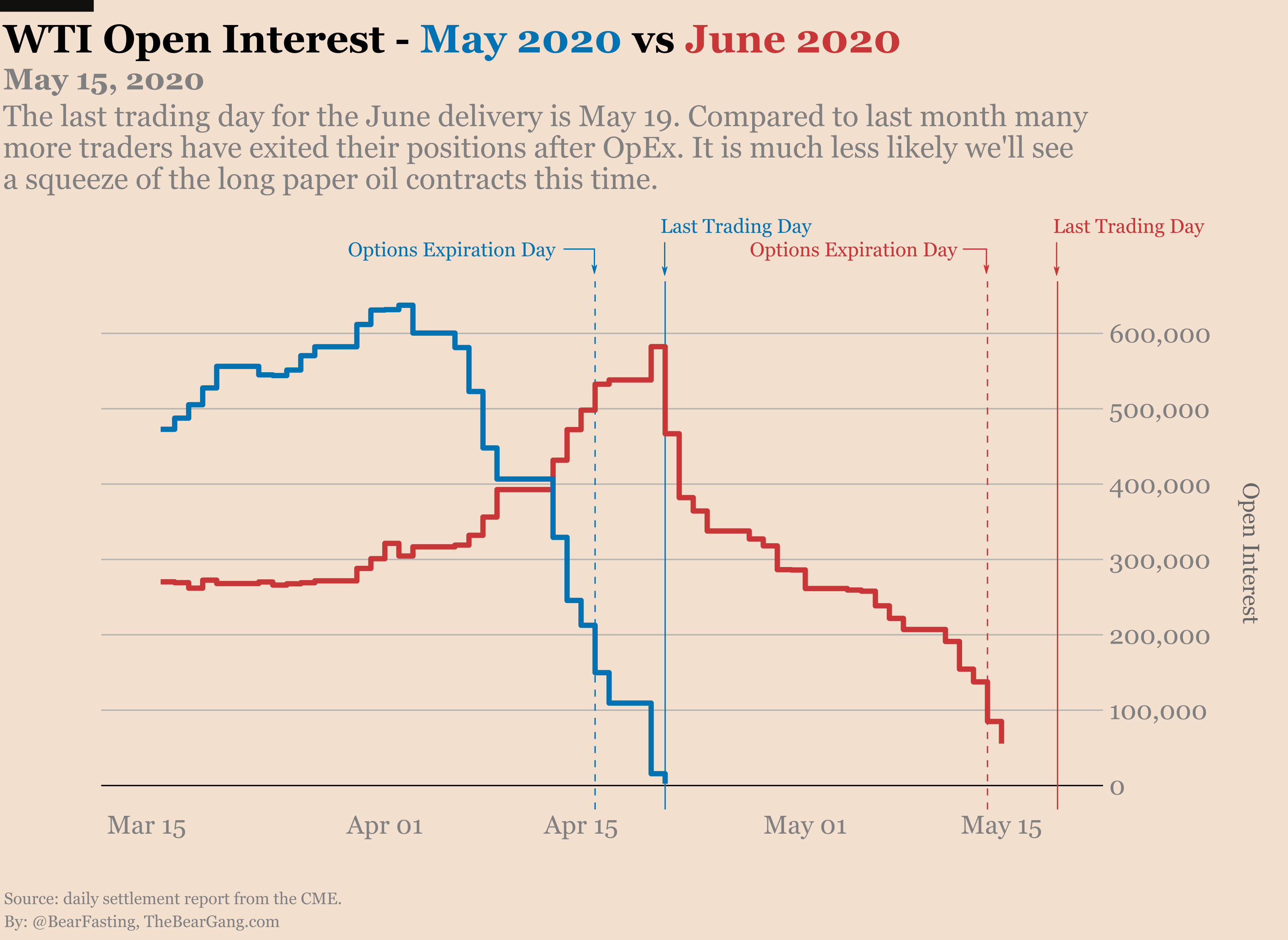

With regard to the immediate concerns for the June delivery prices it looks like the risk of a repeat of negative prices is low.

Looking at the open interest after OpEx last Thursday there aren’t that many positions left on the June contract. And with the super contango gone there is no reason for any long paper oil trader to not roll their contract if they haven’t done so already.

So at first sight it does not look like there will be any strong imbalance between long paper oil contracts and short physical oil traders.

But the oil market is always full of surprise so let’s see how that plays out! The last trading day for the June delivery is on Tuesday.

In the meantime if you liked this article please subscribe and share!