This Week In Oil - May 24, 2020

Game theory...

There was no fireworks for the last trading days of the June delivery.

It looks like traders and everyone else have been scared enough by the negative prices last month to be extra cautious and make sure it didn’t happen again.

As a matter of fact traders were so cautious about the June delivery that it traded above the July contract before it expired!

But that’s for the past. Let’s look at the futures!

First order of business: storage. This has been the key issue driving WTI in the teens.

The market is signalling that the crisis is over. That is clear when looking at the time spreads. In only a few weeks we are back down to $0.4 on the front month and all the way to next year. Below $0.5 is a typical range for those spreads so that signals the market does not foresee more storage issue in the near future.

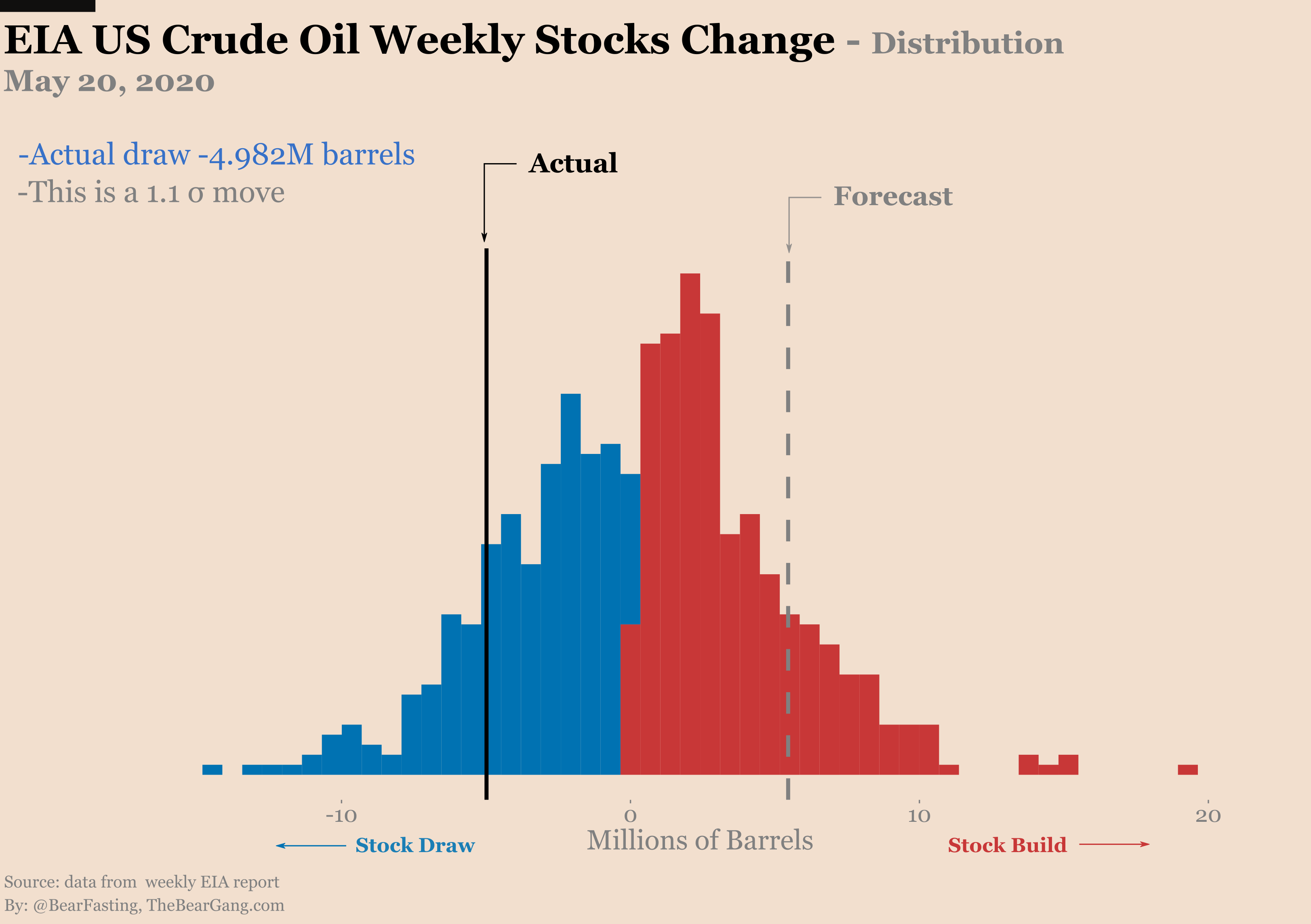

And the storage data from the EIA backs this up. We went from having record builds every week in Cushing to setting record draws. This week:

Cushing drawing -5.6M barrels for a record 3.5 σ move.

Overall drawing -5M barrels for a 1.1 σ move.

Cushing inventories are moving out of the danger zone pretty quickly. At this rate we’ll be back to 50M barrels in a week or so.

So this end of the storage crisis is very real. And after all it makes sense if you consider how full inventories were a couple of weeks ago. If there is no storage space or if storage space starts being so expensive that it doesn’t make sense to produce more then naturally the market is going to respond.

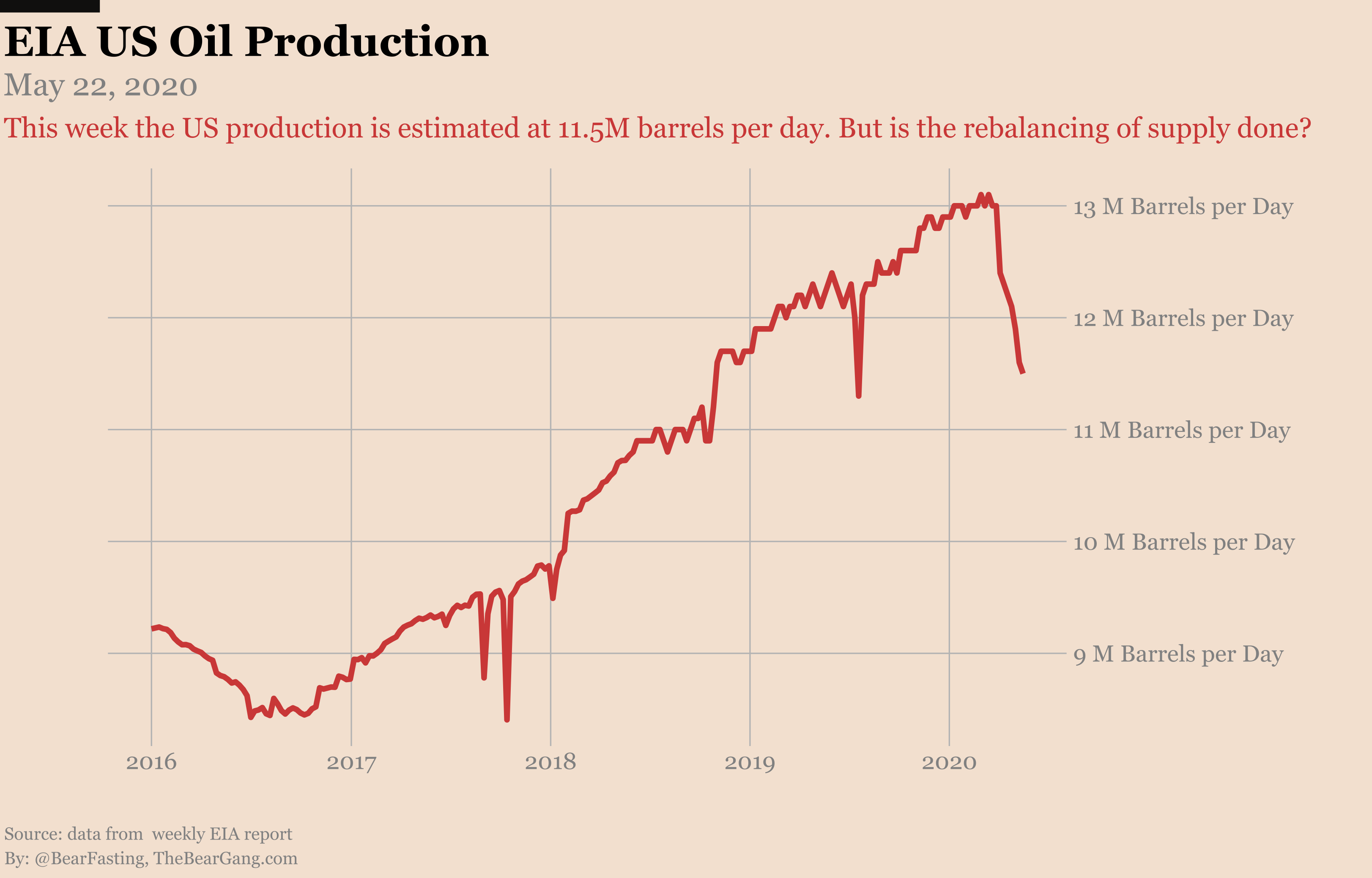

And responding the market did by cutting production to whatever makes sense in terms of demand and storage capacity.

It shows that the market is working. There is no need to impose mandatory shut ins of oil wells. There is no need to orchestrate production cuts at a higher level. In extreme situations the market will adapt.

But that’s a double edged sword. If the conditions are changing you can bet that the US production is going to start pumping again. Let’s think about that for a minute.

This is where the game theory of oil producers comes into play. There are three players in this game:

Shale producers.

Other US producers.

OPEC+ producers.

For sure OPEC+ has a lot of internal dynamics to it. Saudi Arabia and Russia often have different incentives. And the smaller producers are always tempted to play some games to avoid total compliance to the decisions of the organization. But for a high level view let’s consider them as one block for now.

So the situation right now is as follows:

Europe, the US and large parts of Asia are coming out of lockdown.

That means demand is bound to come back online.

Nobody knows how demand will recover. There are way too many uncertainty for that. See for example the fact that China just scrapped their GDP target. When even China who isn’t shy about twisting the stats does not want to set targets you know that something bad is going on.

We don’t know what the demand will be but everyone’s assumption is that there will be some. That means for the oil producers the question is how much share of it can they get.

For Saudi Arabia and Russia — this applies to OPEC+ members in general — the story is simple. They are depending on oil to sustain their budget. So the game for them looks like that: oil price needs to be high enough but should not be too high to destroy demand. Their goal also is to capture as much market share as possible.

That means OPEC+ will start producing more when demand is back. And they want to make sure prices don’t get too high to not give a free meal to the US producers.

The US shale producers don’t have the strongest financials to support them. They certainly have been the ones hurt the most from the oil price crash. But after some consolidations that will surely happen you can be 100% sure that they are going to start pumping again really fast. Storage was the bottleneck and with that gone we don’t need to wait for prices to be back at $50 to see shale activity starting again.

That points towards production restarting sooner rather than later for shale oil.

The rest of the US oil production can’t seat on the side and say “oh wait we don’t really know how big the demand recovery is going to be or really how long that will last so let’s be cautious”. Nope. They need to play the game and align to what the other players are doing.

Again that points toward a bottom in the production being already in place.

For sure if this analysis is correct it will take some times for it to show in the data due to reporting lags. But my point with this high level view of the situation is that production coming back online together with uncertainties on how demand will recover has to put some cap on how far prices can run.

And that’s even without counting on all the floating oil supplies that will have to go somewhere…

In just four weeks WTI is up 65%. With the bullish sentiment running high you have to ask how long this rally can last. For sure you don’t want to bet against the trend.

Still I think this rally is vulnerable to three things:

Production coming back online too fast because of the game theory oil producers are playing.

The demand recovery stopping really fast simply because the global economy is in bad shape, see China.

All those floating oil supplies coming into play.

One thing is clear though, we’ll get more volatility in the short term.

But let’s see how that plays out. In the meantime if you liked this article please subscribe and share!