This Week In Oil - May 31, 2020

Pressure points

You know what? I don’t want to waist your time. So let me keep that short and go straights to the point.

There is nothing new that we have learned over this week that makes me change my mind.

This oil rally is fragile. It is fragile because it stands on very shaky legs.

The US crude oil stocks are still building.

Global trade tensions are back between China and the US.

China has trouble getting back to pre-COVID19 levels of activity.

As lockdown measures are lifted it is becoming clear how much the real economy is suffering.

We are moving away from the fantasy of a V-shape recovery.

Honestly I don’t know how WTI is back to $35 in these conditions. To be fair it isn’t like the oil market hasn’t been under selling pressure last week. But at the end of the day these were just opportunity for the bulls to buy the dip.

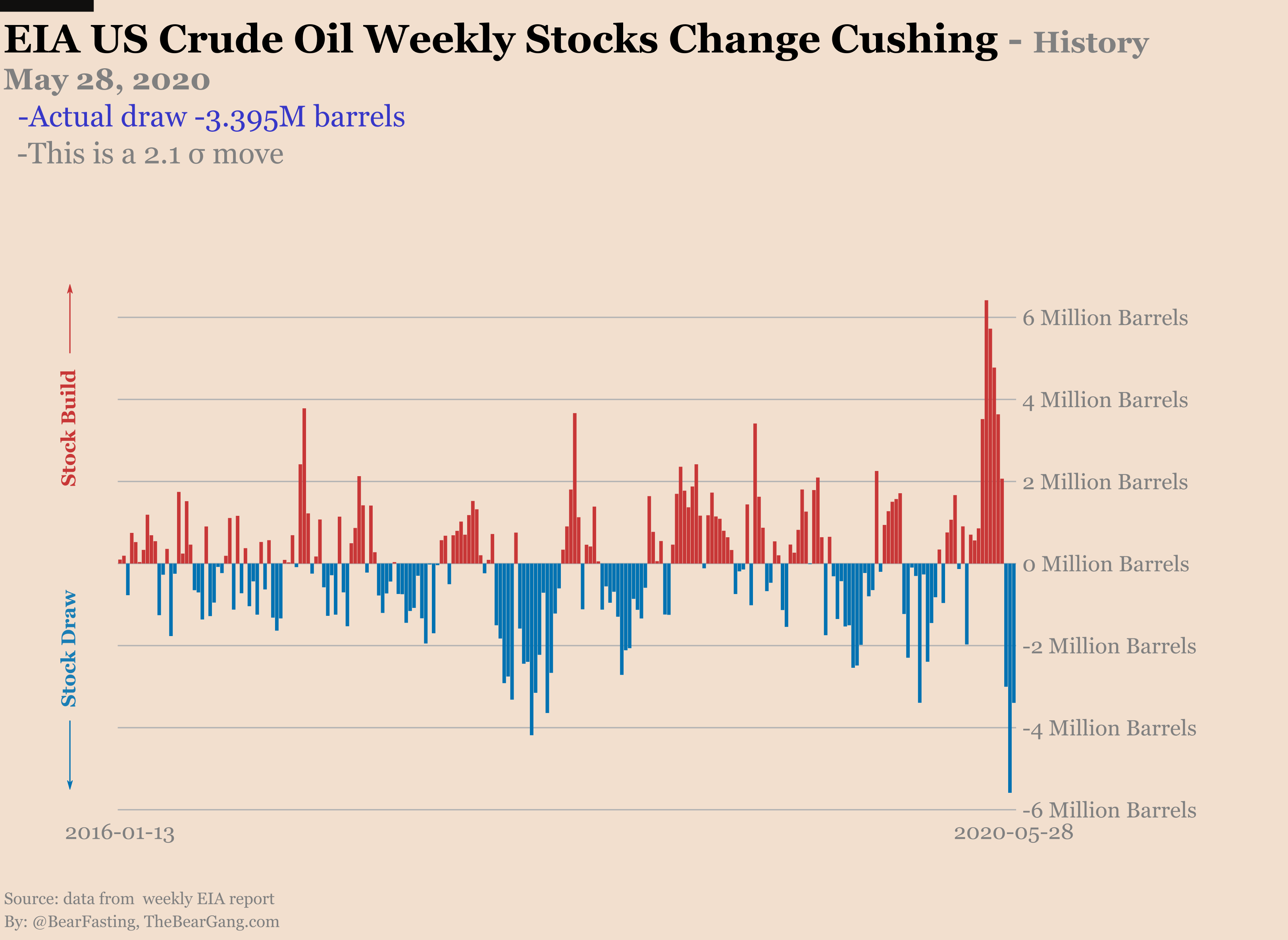

Let’s start with our weekly review of the oil storage situation in the US. The EIA numbers for the week are:

US Crude +7.9M barrels (1.7 σ move).

Cushing -3.4M barrels (2.1 σ move).

Gasoline -0.7M barrels.

Distillates +5.5M barrels.

For sure Cushing had a big draw. But overall in the US oil stocks are on the rise. Part of this rise is due to all that oil on water starting to be delivered to fill on-shore inventories. The pressure from those tanker is massive. I’ve read estimations of a few hundred million barrels that are going to come back to the market in the next few months.

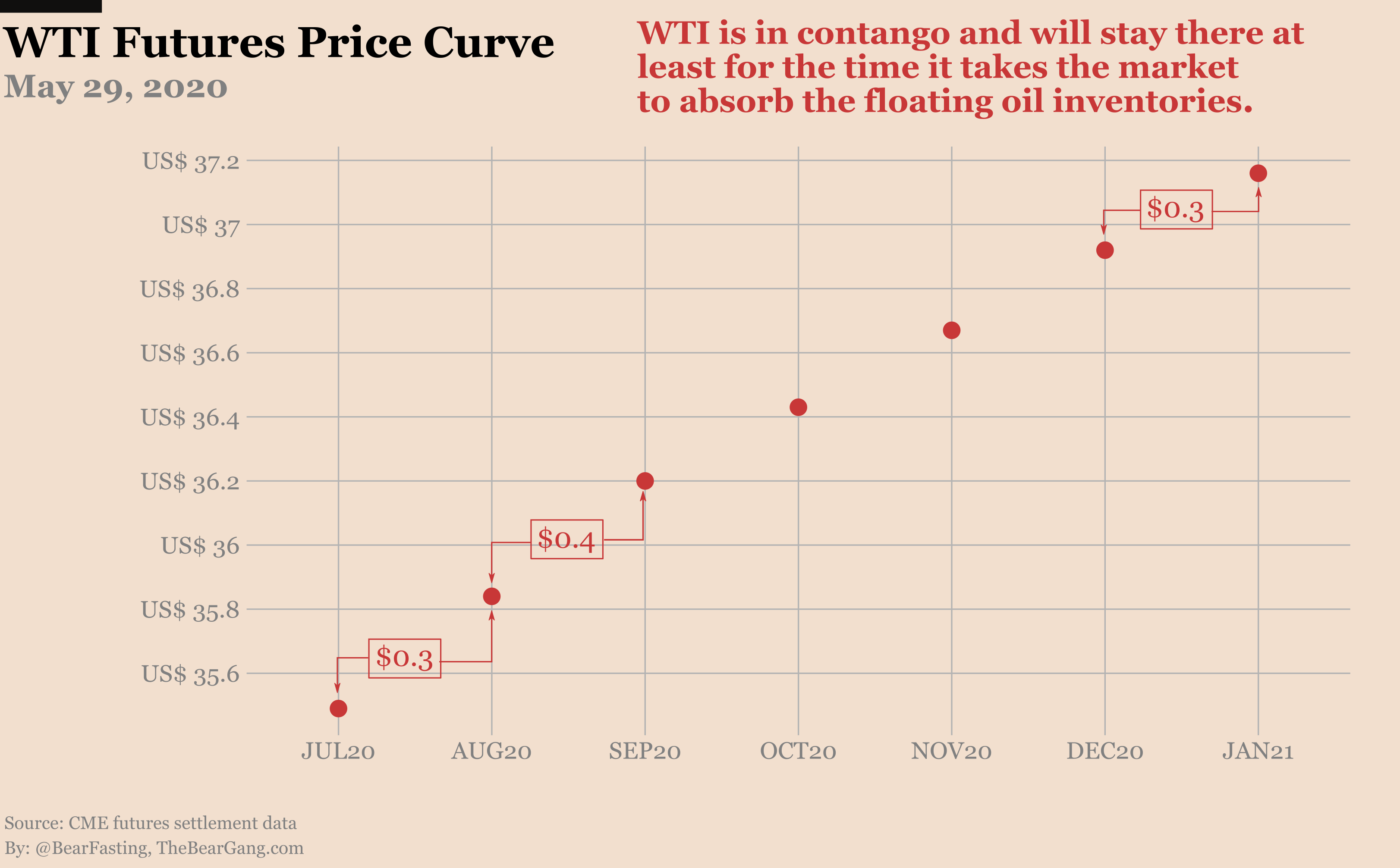

So much floating capacity has to cap the price of oil for a while. With the slow drip of tankers adding to weekly crude oil build for weeks you can be sure we are going to stay in contango for a while.

And talking about oil import, there was an interesting story on Reuters this week. Here is the juicy extract:

“Chinese oil stockpiling is normally driven by state giants which sweep up cargoes to fill the government’s strategic petroleum reserves or commercial reserves held by refiners.

However, in the current downturn, stockpiling has been driven by financial investors who believe oil is set to bounce strongly off its lows, said the second official.”

It seems like the famous rebound of demand from China is in large part driven by… drum roll… more bets that the demand will come back!

So yea, talk to me about the fundamentals being there… even for China, all of this surge of demand is a bet on a V-shape recovery of the economy. There is nothing particularly bullish about that for the long run.

The production is down another 100k barrels in this weeks’s estimate. When we get the actual production numbers we’ll probably see that the production has bottomed now, at least for the short term.

Based on those production cuts estimations together with guesses of how the demand is going to recover many analysts are predicting that already in June production won’t be enough to meet demand.

I think that is way too optimistic. Based on the data we have and the incentives driving the oil producers I’d expect production to start increasing again to match any spike in demand. And if prices are not already too low that would trigger another intense market share war.

So let me summarize what challenges this rally needs to face in order to move forward:

Demand recovery needs to overcome the glut in floating storage.

Demand recovery needs to overcame the high levels of on-shore inventories (way above 5 year range at the moment).

Production cuts need to outlast any rise in oil price.

And it must do all that while avoiding a second wave of the COVID19 and possibly more lockdown orders and destruction of the real economy.

Final assessment: capped price with bearish outlook.

But let’s see how that plays out. In the meantime if you liked this article please subscribe and share!